I’ve heard a lot of conversation about what other organizations are doing, and I think it might serve us better to ask what the practice of tomorrow will look like. What type of practice do we need to build to succeed, hit those moral imperatives, and survive under the business constructs?

While most would agree that radiology practices are undergoing consolidation, many questions remain regarding its extent and the effects, resulting in hype, hyperbole, and not a small amount of uneasiness throughout the specialty.

In an attempt to bring some order to the subject, Randal Roat, FRBMA, Strategic Radiology COO, reviewed the landscape, tallied up the available numbers, and attempted to assess whether consolidation had delivered on its objectives in “Radiology and Independence in a Consolidating World,” a talk presented at the RBMA Paradigm meeting on April 15 in Colorado Springs.

He also shared the results of Strategic Radiology’s “Pulse-Check Survey,” which provided some interesting insights into the mood, challenges, and demographic profiles in radiology practice as provided by the 45 practice executives who participated in the survey.

To begin, Roat reviewed the lexicon of consolidation as well as the current practice models in radiology. In outlining the models, he reviewed the fiduciary obligations of each model, the purposes, the influences, and the radiologist–administrator relationship. “When we look at these models, ownership is important,” Roat said.

In the Academic Practice, the radiologist typically is an employee and the fiduciary responsibility of the practice goes back to the institution. In the Corporate Practice, radiologists are typically employed, although some may be primarily non-governing shareholders, with a fiduciary responsibility to shareholders and investors. In the Hospital-employed Practice, employed radiologists have a fiduciary responsibility to the institution, and there is a distinction between the purpose of for-profit and non-profit hospitals. In the Independent Practice, radiologists are shareholders and the fiduciary responsibility is to shareholders and patients; likewise, in the Affiliated Practice Model, assemblages of aligned private practices, responsibility is to shareholders and patients, but the obligation is to multiple groups, not one.

Relationship and Mission

Given that the audience was primarily non-physician practice executives, Roat spent time delineating the physician–administrator relationships associated with the different models:

His assessment of the various practice model missions was based on a review of their web sites.

Academic institutions promote new approaches to medicine, improved outcomes, and access through multiple locations in the case of the UCLA Health System.

The corporate practices advertise their goal to transform medicine and use related terminology on their web sites, including next generation, leading the way, transformation, investment, and growth.

Representing the hospital-employed radiology model, Sutter Health focuses on the medical team, state-of-the-art technology, and expert care that can be obtained close to home.

A review of several Strategic Radiology independent practice member web sites yielded a focus on patients, health and well-being, and community.

Web sites of several affiliated practice models—including Strategic Radiology—focused on collaboration, best practices, quality improvement, cost reduction, scale, and efficiency.

Consolidation Drivers and Options

Opportunity was at the top of Roat’s list of consolidation drivers. “Radiology is fragmented and there is opportunity in this industry, so capitalizing on this opportunity is a reason,” he said. To illustrate the opportunity that consolidators see in radiology, he shared the following data points from a Coker 2018 Industry Spotlight report:

Another commonly cited factor fueling the consolidation trend is an increasingly complex business and regulatory environment. “Some people are saying, ‘Look, I just want to tap out of this,’” Roat speculated.

Fear, uncertainty and doubt, including the fear of missing out on capitalization opportunities, are causing some practices to choose to sell to a consolidator, and in some cases, a practice may not see another path. “For some very large practices that have scaled to a region, scaled to a state, the next evolutionary step might be scaling nationally,” he said. “They may feel they need some assistance, some business support, and some financial support.”

Finally, there is the green reason. “Everybody says, ‘Yeah, they want the money,’ and to an extent that is true,” Roat said. “I also think there are a lot of other factors that go into this decision, and you can’t tie it just to one of them.”

Objectives and the Practice of the Future

Quite a few radiology practices have grown organically over the past several decades in response to health system growth, and also through mergers and acquisitions to achieve greater scale, access to technological resources, and to be able to provide more subspecialized services around the clock. Roat enumerated other objectives cited by consolidators as benefits of scale: More resources, ability to invest in technology, data aggregation, population health, and the efficiency of corporate governance.

With multiple courses of action available to independent practices—maintain status quo, merge or affiliate with other independent groups, align with a hospital, or sell to a consolidator—Roat suggested taking a pause to consider what the ideal practice of the future should look like.

“I’ve heard a lot of conversation about what other organizations are doing, and I think it might serve us better to ask what the practice of tomorrow will look like,” he suggested. “What type of practice do we need to build to succeed, hit those moral imperatives, and survive under the business constructs? If you look at it that way, the questions then become: Do we build our practice? Do we reinvest in our practice? Do we monetize our practice?”

Roat recommended reviewing the ACR’s Imaging 3.0 resources, which provide a roadmap to value-based practice and supports radiologist leadership and a patient-centered, integrated care model; demonstrates a consultative role for radiologists; and is hallmarked by quality, appropriateness, safety, efficiency, and patient satisfaction.

He also directed attendees to a document co-created by the ACR and the RBMA called Most Valuable (Radiology) Practice.

“This is what clinician leadership has identified as a pathway to move forward,” Roat said. “As the business guy, I become focused on how we make all of this happen, but ultimately it is the radiologists who can provide direction for where their company, that is designed to practice medicine, should go.”

Corporate Consolidation

In taking a deeper dive into corporate consolidation, Roat shared the following data on general physician M&A activity from PriceWaterhouseCooper:

“Physician acquisitions out-paced hospital acquisitions in 2018, so that is a lot of activity,” Roat observed.

We’ve also seen an increased number of radiology practice acquisitions by corporate consolidators in the past two years, Roat noted. Since the start of 2017:

A Changing Radiology Landscape

Roat reviewed a recent analysis published in the Journal of the American College of Radiology that showed a decline in the total number of radiology practices as well as a trend toward larger practice size. Based on an analysis of PECOS data from 2014 and 2018, this article by Rosenkrantz et al offers further evidence of consolidation activity within the radiology market.

During the same time period, the number of radiologists practicing in groups of less than 50 declined, while those practicing in groups of 50 or more either remained stable or increased:

Whether or not consolidation has delivered on its objectives is harder to assess, Roat acknowledged. “By and large, it is probably still too early in radiology to say,” he said.

He did, however, point to a peer-reviewed report on the experience in dermatology, an early target of private equity firms, that raises concerns about the fiduciary obligations of corporate practices, evidence of quality declines and higher patient cost, as well as practice failures.

Roat referred to an article published in the Journal of the American College of Dermatology by Konda et al that provides data supporting the hypothesis that private equity had targeted for acquisition outlier dermatology practices that performed a greater than average number of high-dollar procedures, such as intralesional injections and skin biopsies

The same article created a storm of controversy when it was pulled, reportedly under pressure from members of acquired practices including the incoming president of the American College of Dermatology, according to an article in the New York Times.

Radiology Pulse Check

Toward the end of his talk, Roat invited Anthony Werner to the podium to present the results of a Pulse-Check survey that Strategic Radiology distributed via three email blasts to RBMA membership. Werner is a director at Minneapolis-based CliftonLarsonAllen, which tabulated survey results.

The survey received 45 responses from eight radiologist leaders and 37 practice administrators. Most represented independent practices, but 6.5% were from corporate-owned practices and 4.4% identified as out-sourced administrators, likely employed by billing MSOs.

Overall, the survey provides some interesting insights into practice priorities, needs, and the concerns that are keeping practice leaders up at night. Werner shared the following key takeaways from this snapshot:

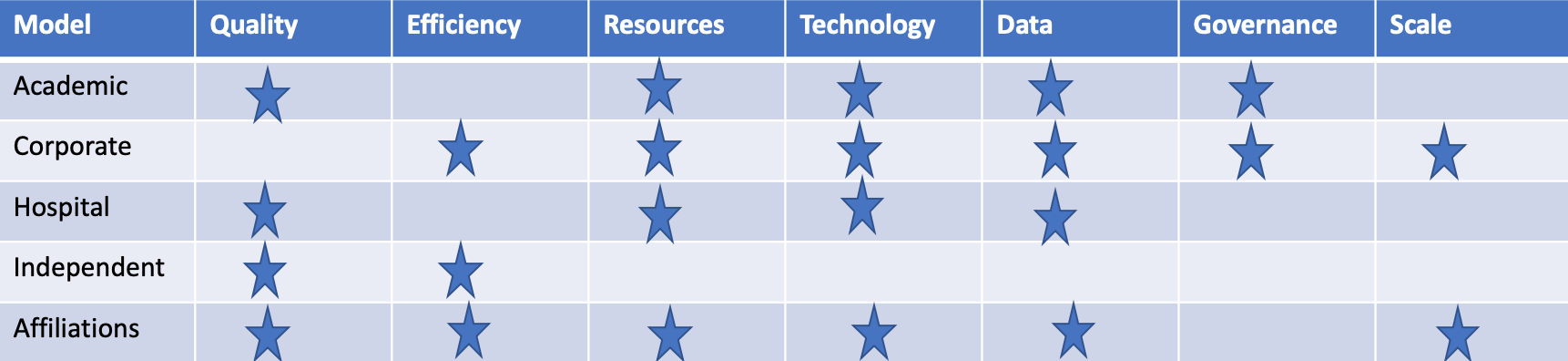

Finally, for discussion purposes, Roat created what he called a strawman grid that assessed the potential ability of the different models to deliver on quality, efficiency, resources, data, governance, and scale. Admittedly, the assessment was non-scientific and highly subjective. As one might predict, the grid created much conversation and collegial disagreement, perfectly reflecting the current state of radiology.

Hub is the monthly newsletter published for the membership of Strategic Radiology practices. It includes coalition and practice news as well as news and commentary of interest to radiology professionals.

If you want to know more about Strategic Radiology, you are invited to subscribe to our monthly newsletter. Your email will not be shared.